One in eight women will develop invasive breast cancer over the course of her lifetime,1 and 85% of breast cancers occur in women who have no family history of breast cancer.2 Such a diagnosis can be scary. For employees with a High Deductible Health Plan (HDHP), it can feel overwhelming.

The Role of an HDHP

While HDHPs do offer lower cost alternatives for employers, many employees may be uneasy about the direct affect an HDHP can have on their finances. Premiums will likely decrease under this type of plan, but out-of-pocket costs may increase—opening the door for potential gaps in coverage.

If you’ve considered making the switch to an HDHP, supplemental benefits may help you balance employee coverage with rising healthcare costs.

Bridging Coverage with Cancer Insurance

Limited Benefit Cancer Insurance from American Fidelity Assurance Company is one of several supplemental benefits products that may help your employees manage higher deductibles.

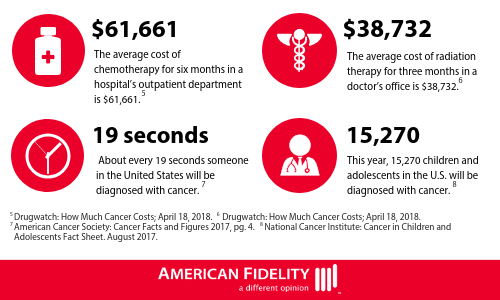

New cancer cases in America are diagnosed at the rate of about 4,626 per day3,which means one or more of your employees may come face-to-face with an unexpected diagnosis. If they, or a covered spouse and/or dependent, are diagnosed with cancer, the financial costs can be overwhelming.

Because cancer insurance is separate from traditional major medical plans, it may provide your employees with additional benefits to cover an unexpected diagnosis—all at no additional cost to your bottom line.

Cancer insurance benefits are paid directly to the policyholder, which means they can use the money where it’s needed most. Whether it’s the medical costs of chemotherapy and radiation, or everyday living expenses, cancer insurance can help if diagnosed with a covered cancer.

Catching Potential Problems Early

Because between 30-50% of cancer cases are preventable,4 annual screenings and tests may help catch potential problems before they arise.

American Fidelity’s cancer policy includes an annual diagnostic testing benefit. Cancer policyholders receive yearly reimbursements for eligible tests, like mammograms and colonoscopies. And with AFQuickClaims™, all eligible wellness and diagnostic testing claims could be paid in as little as one day when enrolled in direct deposit.

If your business is making the switch to an HDHP, employee preparation is key to a successful transition. Offering supplemental products—like cancer insurance—and providing benefits education may help your employees manage their deductibles, while you manage your bottom line.

This blog is up to date as of September 2018 and has not been updated for changes in the law, administration or current events.